Issue Brief - Internationalization of the RMB: An Emerging Competitor to the US Dollar

An in-depth look at geopolitical and economic trends

By: Jessica Yoon

Welcome back to the TSG Issue Brief, where we take an in-depth look at geopolitical and economic trends. Jessica Yoon thoroughly examines the trends shaping the growing role of the renminbi and offers an outlook for its continued rise but cautions it is still constrained as a replacement for the US dollar.

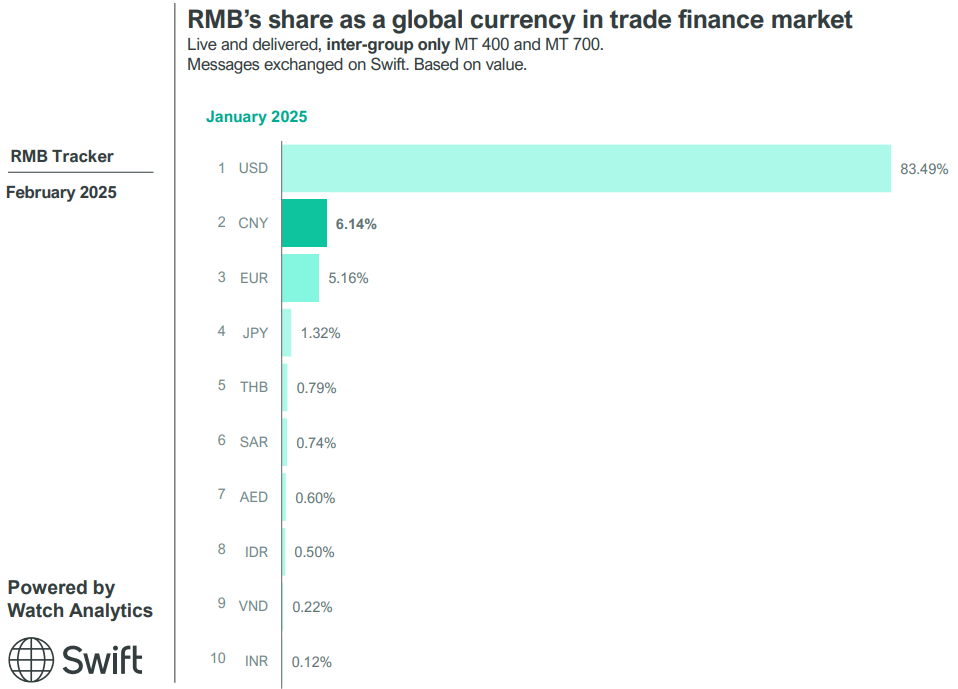

Geopolitical tensions, US protectionist policies, Western financial sanctions, and China’s desire to be a more consequential player in international financial affairs have accelerated China’s push to promote the renminbi (RMB) as a global currency and reduce international reliance on the US dollar (USD) and Western financial systems. Beijing’s efforts to internationalize the RMB coincide with a broader “de-dollarization” trend that China also seeks to exploit. Concerns over existing and potential US-led sanctions (e.g., those targeting Russia after the Ukraine invasion) have prompted many countries to seek alternatives to the USD to insulate themselves from US financial pressure. Sanctioned states and their partners have increasingly turned to local currencies and alternative payment systems. Russia’s exclusion from SWIFT spurred greater use of China’s RMB for bilateral trade, lifting the RMB’s share of global trade finance from under 2% before 2022 to 6.1% in 2025 (still a distant second to the USD at 83%).

To expand its global footprint, Beijing has promoted RMB trade invoicing, extended currency swap lines, built payments infrastructure, and launched a digital currency. It has also leveraged international forums such as BRICS to advocate trade settlement in local currencies, not only promoting the RMB but also marketing local currency use as part of a broader strategy to erode USD dependence across emerging markets. At the same time, volatility in US policies has undermined confidence in the USD, bolstering interest in currency diversification and aligning with China’s strategic goal to reduce its own USD dependence and expand the RMB’s global use. Beijing has explicitly advocated a more multipolar international currency order, positioning the RMB’s rise as a linchpin of that vision.

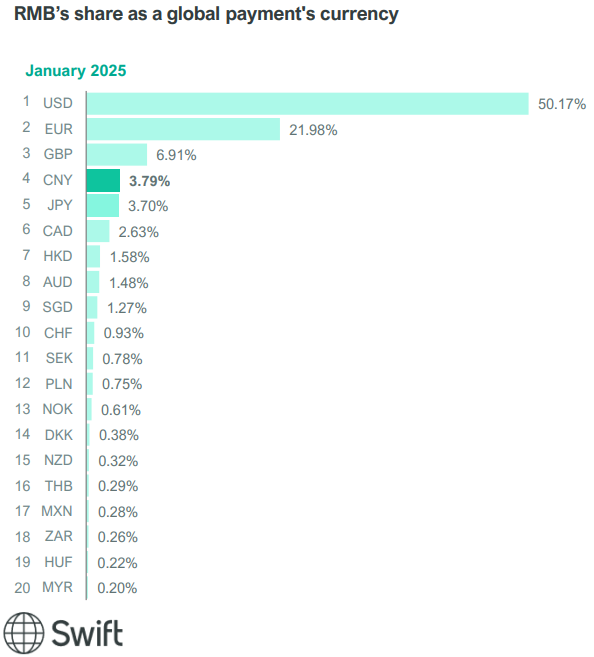

But wider adoption of the RMB remains constrained; it ranks 4th among global payment currencies at 3.79% after the USD (50%), EUR (21%), and GBP (6.9%). China’s strict capital controls, limited financial transparency, and the absence of safe and transferable RMB-denominated assets for international investors continue to impede its full globalization, leaving the USD still dominant.

Surge in RMB trade settlement and payments

China has rapidly expanded RMB use in cross-border trade settlement. In the first quarter of 2023, the RMB overtook the USD in China’s trade transactions for the first time, with 53% of China’s cross-border trade settled in RMB vs. 43% in USD, a reversal from a decade prior when the USD made up more than 80% of China’s trade payments. This shift has been fueled by China’s trade partners (especially in Asia, Africa, and sanctioned states) accepting RMB for exports to China, as well as Beijing’s encouragement of RMB invoicing for imports. (RMB settlement now accounts for about 26% of China’s goods trade, up from 15% before 2022.) Energy trade is also slowly diversifying – Gulf oil exporters, most notably Saudi Arabia, have discussed pricing oil in RMB as China becomes a top buyer, with Beijing strengthening its financial ties through a $7 billion currency swap agreement with Riyadh.

While the RMB’s overall share of trade finance remains modest, its rise to the second-most-used trade finance currency has been exponential, and its growth is expected to continue as more emerging economies integrate with China’s financial infrastructure. Much of the growth stems from China’s Global South trading partners opting to settle trades in RMB, especially where Western banks have withdrawn or where USD costs have risen. More non-Western countries, including Argentina and Brazil, are using RMB for imports from China and even some inter-regional trade.

While the RMB’s international use is expanding, the USD remains unchallenged as the dominant reserve and settlement currency. Chinese companies and banks, with the encouragement of Beijing, policymakers, have nonetheless embraced the RMB for international dealings. The share of Chinese non-bank companies’ cross-border transactions conducted in RMB surged to about 50% in 2023, reflecting both policy incentives and the RMB’s growing acceptance abroad. Major state-owned enterprises have been instructed to favor RMB in contracts where feasible. Meanwhile, foreign central banks have increasingly signed currency swap deals or established RMB clearing accounts, including Brazil ($27.7 billion) and Thailand ($9.7 billion) in 2025, making it easier for their local firms to invoice and pay in RMB. These trends show the RMB carving out a role as the leading non-dollar currency for trade, particularly in the Global South, even as the USD remains dominant worldwide.

Financial infrastructure: CIPS and swap lines bolster RMB use

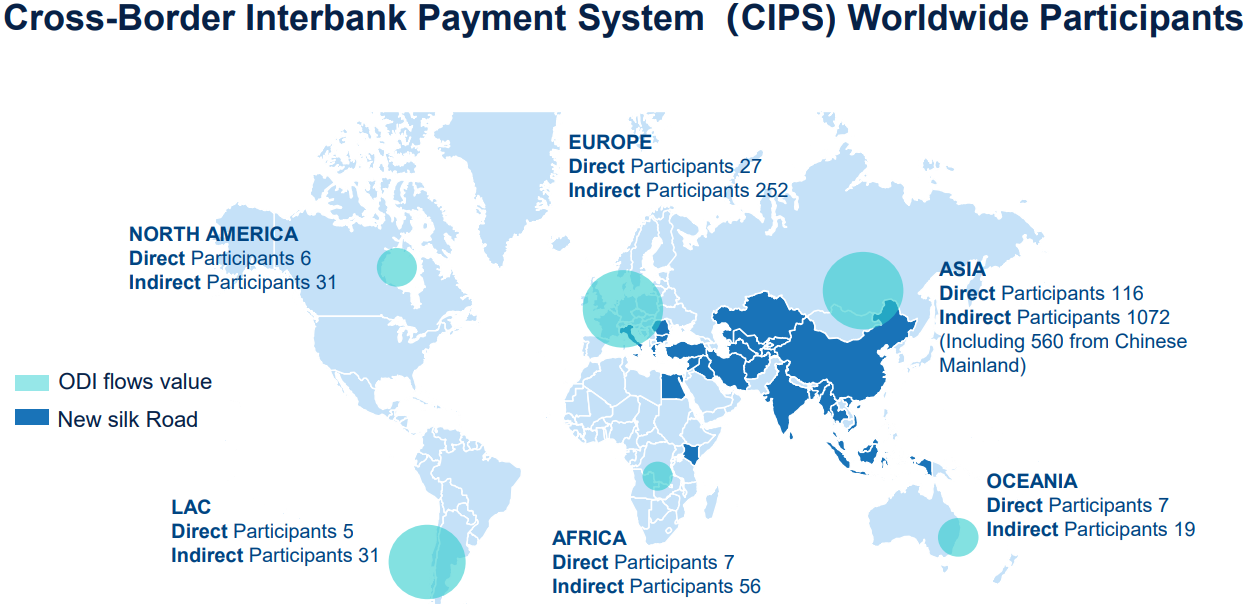

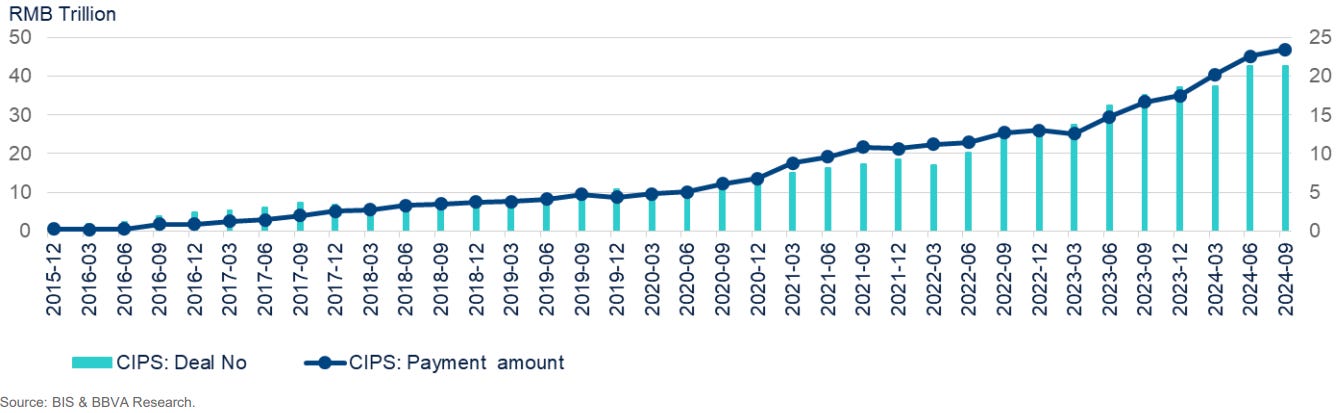

China has constructed a financial infrastructure to support greater RMB use internationally. A pillar of this effort is the Cross-Border Interbank Payment System (CIPS) – China’s alternative to -based networks like SWIFT (financial messaging) and CHIPS (dollar clearing). CIPS, launched in 2015, allows banks worldwide to clear and settle payments in RMB. The network has expanded steadily: by 2024, CIPS had 168 direct participant banks and 1,683 indirect participants across 119 countries, a 20% increase in participants from the year prior. Notably, 76% of new CIPS members in 2024 were overseas banks, indicating rising global connectivity to China’s system. CIPS handled a record 8.2 million transactions in 2024 (up 24% yoy) as more banks routed cross-border payments through the RMB network.

CIPS cleared $24 trillion in total transaction volume in 2024, a 43% increase from 2023. While still much smaller than SWIFT/CHIPS (which handles about $1.8 trillion per day in dollar payments), CIPS’s rapid growth underscores its rising importance. Critically, CIPS provides an alternative messaging and settlement channel insulated from potential Western sanctions. Its use spiked after Russian banks were barred from SWIFT in 2022. In addition to using Russia’s own alternative, SPFS, Russian institutions shifted a large volume of payments onto CIPS, contributing to a 21% increase in CIPS settlements that year. China has promoted CIPS as a neutral platform, with dozens of regional banks joining to facilitate RMB clearing (e.g., African Export-Import Bank, the Central Bank of the UAE, Bangkok Bank).

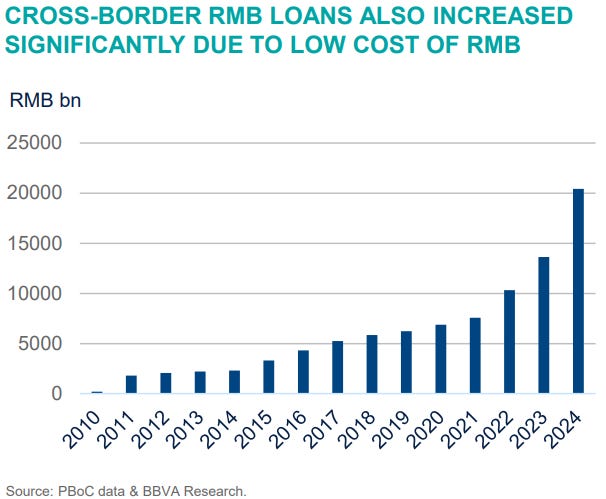

Another key tool is China’s extensive network of bilateral currency swap lines. The People’s Bank of China (PBOC) has swap agreements with the central banks of over 30 countries, totaling roughly $590 billion in swap facilities. These allow foreign central banks to exchange their local currency for RMB, providing liquidity to local banks and importers for RMB-denominated trade. Since 2009, China has steadily expanded these swaps to support trade settlement in RMB; it is also being used as a form of emergency lending (e.g., including to markets during COVID-19 disruptions). Beijing has used swaps and direct loans to act as a “lender of last resort” in RMB. In recent years, China extended sizable RMB liquidity support to distressed borrowers to help them avoid default and keep projects financed; in April, for example, Argentina renewed a $5 billion portion of a yuan swap line. This has the dual effect of encouraging greater RMB use in those countries and laying groundwork for the RMB as a reserve currency in their central banks. China is leveraging its financial ties – through swap lines, development loans, and the Belt and Road Initiative (BRI) – to internationalize the RMB by embedding it in trade, finance, and aid relationships.

The digital yuan and fintech pathways

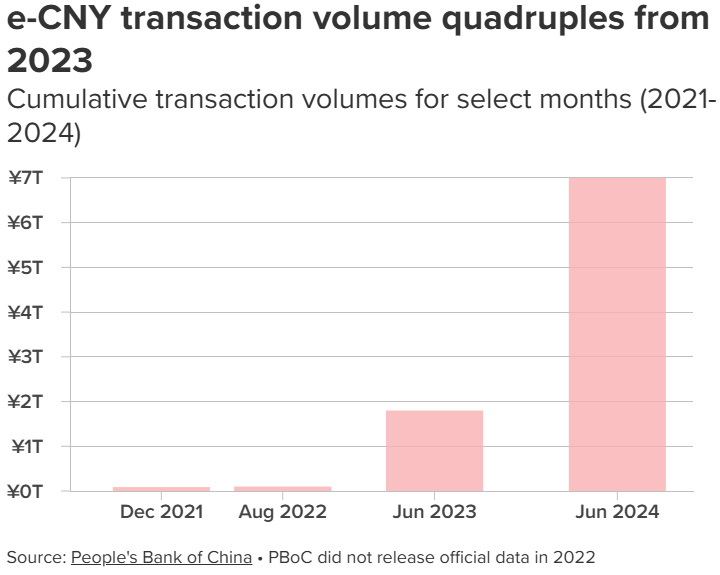

China’s embrace of financial technology is providing new avenues to promote the RMB globally. Foremost is the digital yuan (e-CNY), China’s central bank digital currency (CBDC). The e-CNY, still in the pilot phase, is the world’s largest CBDC project. By mid-2025, cumulative e-CNY transactions reached $7.3 trillion across over 29 cities. The $6 trillion increase in volume yoy reflects rapid adoption in domestic retail use, including sectors ranging from transit fares to government stimulus payments. While primarily focused on internal use and financial inclusion, China has begun testing cross-border payments with digital yuan in collaborations like Project mBridge. These pilots aim to enable instant, low-cost transfers between countries using CBDCs, potentially bypassing traditional correspondent banking networks. A successful rollout could make it easier for foreign businesses and tourists to use RMB digitally without Chinese bank accounts, thus expanding RMB usage abroad. (Meanwhile, the Trump administration has discouraged progress toward a US digital dollar; Trump’s 2025 “Strengthening American Leadership in Digital Financial Technology” executive order and the “Anti-CBDC Surveillance State Act” prohibit federal efforts to issue or promote a US CBDC.)

Beijing is promoting the digital yuan as a hedge against US-controlled payment systems. A digital RMB widely used in cross-border payments (e.g., BRI projects or through overseas Chinese firms) could reduce exposure to SWIFT or dollar clearance networks, offer an alternative for global transactions, and lower costs (e.g., reduce the compliance and correspondent-banking costs embedded in other networks).

However, significant barriers remain before the digital yuan can meaningfully chip away at the USD’s role – including achieving interoperability with other systems and building trust in its security and privacy features. Still, China’s head start in launching a usable CBDC (most major economies are far from issuance) positions the RMB to gain a first-mover advantage in the future digital currency landscape. Alongside the e-CNY, Chinese payment platforms (e.g., UnionPay, WeChat Pay) are expanding abroad, and new multilateral digital payment projects (e.g. African and ASEAN QR code networks) are connecting with China’s systems – developments that could incrementally boost RMB-based transactions over time.

Across the fintech industry, Chinese companies are pushing for RMB-pegged stablecoins to promote wider RMB use abroad. Hong Kong’s 2025 stablecoin regulatory framework may allow fully-reserved stablecoins pegged to the offshore yuan (CNH). Firms like JD.com and Ant Group have applied for Hong Kong stablecoin licenses and are lobbying Beijing to authorize CNH-backed stablecoins, seeing these as useful for e-commerce and trade settlement. Their push reflects concern that USD stablecoins like USDT have gained traction with Chinese exporters (over 99% of global stablecoin volume is USD-denominated), and without yuan alternatives, USD-pegged stablecoins could become the default for cross-border digital transactions and further reinforce USD reliance. An offshore yuan stablecoin could facilitate 24/7, low-cost transactions outside traditional banking – complementing the official e-CNY by serving overseas merchants and investors who require a freely transferable RMB token. If approved, a CNH stablecoin could bolster yuan usage in digital commerce networks that currently default to the USD. Together, China’s digital currency initiatives, payment networks, and swap lines form a multi-layered strategy to chip away at dollar infrastructure and promote the yuan as a viable alternative.

RMB in regional frameworks: BRICS+, BRI, and bilateral deals

Beijing is also leveraging regional blocs and partnerships to broaden RMB usage, especially among countries seeking an alternative to Western-led systems. In the BRICS+ circle (Brazil, Russia, India, China, South Africa, Saudi Arabia, Egypt, United Arab Emirates, Ethiopia, Indonesia, and Iran with additional partners), the yuan’s profile has grown markedly. Trade between China and sanctions-hit Russia is now overwhelmingly conducted in local currencies; by 2024, more than 95% of the transactions were settled in yuan and rubles, and China-Russia trade reached a record $237 billion, a 3% growth year-on-year. Over 40% of daily FX trading volume on the Moscow Exchange is now in yuan, surpassing the USD’s share, and by late 2023, Russian banks held more yuan ($68.7 billion) than USD ($64.7 billion) in deposits. Other BRICS members are also exploring greater RMB use. Brazil signed a pact in 2023 to settle China trade in yuan and reais, establishing a yuan clearing bank in Brazil, and Indian refiners have used yuan for Russian oil purchases. Such moves reflect a broader interest among major emerging economies to reduce USD reliance. Leaders openly endorsed using non-dollar currencies for trade at the 2025 BRICS+ summit.

The BRI is another major conduit for RMB internationalization. China increasingly issues loans and contracts in RMB for BRI infrastructure projects, shifting away from USD funding to minimize currency risk. Many BRI partner countries now hold RMB obtained from project disbursements and trade, which they can use to import Chinese goods. To support this, China set up RMB clearing arrangements across the developing world. For example, a clearing bank and swap line enable Pakistani importers to pay China in yuan. Pakistan in 2023 made its first-ever oil import payment in RMB (buying discounted Russian crude) to conserve USD. While the USD finances the bulk of BRI transactions of up to 75%, the trend toward RMB-denominated projects is growing, creating regional pockets of yuan liquidity.

RMB and commodities

The RMB is now more significant in global energy trade. China, the world’s biggest oil importer, is gradually shifting some oil and gas purchases into RMB. Russia and Iran accept yuan for much of their oil exports to China, with Chinese buyers paying for Iranian crude in RMB via small banks. Iran uses those RMB proceeds to purchase Chinese goods or invest in China, as the currency is not widely accepted elsewhere. In 2023, the UAE completed its first LNG trade with China in RMB through the Shanghai Petroleum and Natural Gas Exchange. This was followed by talks between Saudia Arabia and China on pricing a portion of oil sales in RMB instead of USD – a move that, if realized, could mark a significant shift from the Petrodollar system toward a “Petroyuan” framework.

Additional efforts to circumvent Western sanctions and USD oversight include China and partners reviving barter trade mechanisms for commodity deals, a significant return of Cold War-style exchanges. In August, officials and businessmen in Moscow and Beijing began drafting plans for commodity barter deals – e.g., steel and aluminum in exchange for engines – to avoid payment clearance delays and exposure through conventional financial channels. Barter trade, by definition, sidesteps currency use entirely, but it highlights the lengths China and partners are exploring to reduce dependence on Western-controlled financial systems. If implemented, barter deals will be niche transactions, but they could reinforce broader efforts (RMB settlement, greater use of local currency, small local banks, CIPS, etc.) to make trade sanctions-resistant.

Outlook: Incremental gains, no imminent replacement

The RMB’s internationalization is clearly advancing. In trade, finance, and technology, the groundwork laid by Beijing is boosting the RMB’s global usage, and the RMB is now the leading non-Western currency in cross-border trade. China’s ability to offer an alternative development model – through initiatives like BRI funding in RMB and emergency lending – further promotes use of its currency. Over time, if these trends continue, more of the world’s commerce and financial flows are likely to be settled in RMB, reducing (at the margins) the ubiquity of the USD.

However, Beijing’s policy choices impose fundamental structural constraints on the RMB’s internationalization. China maintains tight control over capital flows and the exchange rate, prioritizing domestic financial stability over full currency convertibility; this limits foreign demand for RMB assets. China’s currency is not widely convertible, and its financial markets lack the depth and openness of those in dollar economies. China must offer broad, liquid markets and strong legal protections – areas where it needs progress to further internationalize the RMB, but there are no signs Beijing will accept the risks of a freely floating RMB or fully liberalized capital account. (Watch for some signs of increased openness in the 15th Five Year Plan set to begin in 2026.) Without those reforms, the RMB cannot become a true global safe-haven currency. Additionally, China’s recent economic troubles (slowing growth, property sector strains) and authoritarian governance may deter foreign investors from holding RMB long-term. China’s reluctance to open its tightly managed financial system remains a key obstacle to building international confidence.

The USD’s dominant position remains secure for the foreseeable future. The US currency still underpins the bulk of global reserves, debt issuance, and payment networks. No other economy – including China’s – offers the same combination of economic size, market credibility, rule of law, and currency stability that undergirds the USD’s status. Even as strategic competition spurs efforts to diversify away from the USD, the network effects and trust in the dollar-built system are hard to undo. In practice, the RMB’s rise parallels rather than replaces the existing order, supplementing it by providing additional currency options and contributing to a slow diversification of currencies in trade and reserves. But even if the RMB is not a near-term competitor to USD’s status as the global reserve currency, the fact that it increasingly facilitates an ecosystem that is separate from the US and Western financial architecture is strategically significant. As an alternative trading and settlement currency, especially for sanctioned states or countries seeking to hedge against US financial pressure – including through tariffs increasingly used as punitive tools – the RMB’s role is expanding. This trend reflects and reinforces the broader push for trade and currency diversification, with China’s pre-existing financial architecture making the RMB a leading non-Western option despite its structural drawbacks. The RMB’s trajectory is continuing upward, with its internationalization representing an emerging parallel to USD dominance – one that reflects an evolving multipolar economic landscape even if the USD-led system remains predominant.

| A guest post by

|