Issue Brief - Export Controls Beyond Security: Implications for Geopolitics and Global Business

An in-depth look at geopolitical and economic trends

By: Jackson Mariani

Welcome back to the TSG Issue Brief, where we take an in-depth look at geopolitical and economic trends. Jackson Mariani explores the increasing use of export controls as strategic tools in global competition and discusses the implications for geopolitics and businesses.

Economic statecraft is central to geopolitical competition, with major powers increasingly relying on coercive trade-based tools to advance strategic objectives. Today, roughly 20% of global seaborne crude oil is sanctioned, tariffs apply to nearly a fifth of global imports, and the number of sanctioned individuals globally has surged to over 70,000 – a 370% increase since 2017.

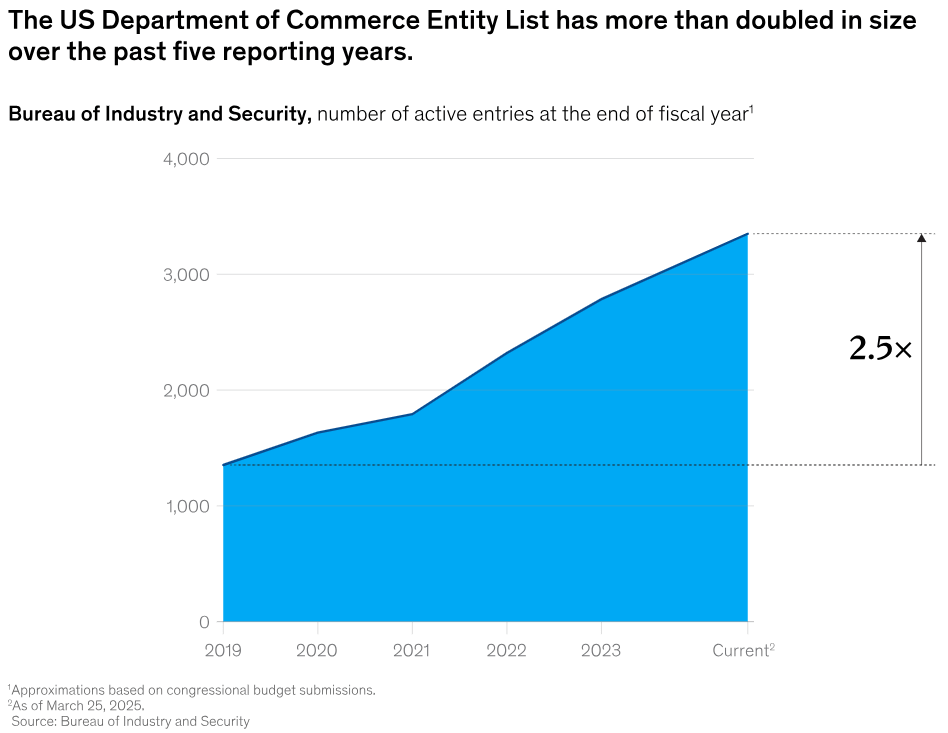

Export controls are among the most consequential of these tools. US export controls now extend beyond their traditional focus on sensitive military and nuclear technology to a wide range of dual-use commercial goods – including semiconductors, advanced manufacturing equipment, critical minerals, and chemical precursors – while the Department of Commerce Entity List expanded from less than 1,000 entries in 2019 to roughly 3,300 in March 2025. Globally, the number of critical raw materials subject to at least one export control measure rose from less than 4,000 in 2009 to over 17,000 in 2024.

The strategic utility of export controls is evident at the highest levels of geopolitics. Semiconductor and critical mineral controls remain a central feature of US-China competition, with the May 2026 Trump-Xi summit offering little clarity, though on critical minerals, the Chinese reiterated that Beijing “implements export controls on rare earths and other critical minerals in accordance with law and regulations, and reviews compliant, civilian-use license applications,” in effect a restatement of their operating procedures. EU controls on exports to Russia – reducing export flows by 54% relative to 2021 – have not only constrained Moscow’s access to war-enabling dual-use technologies but also imposed tangible economic pressure intended to facilitate a negotiated end to the conflict.

Export controls are already central to geopolitical competition, but their impact will grow as multilateral coordination gives way to fragmented national regimes, creating significant consequences for global business.

Legacy export control regimes

The scale and complexity of this fragmented export control environment contrasts with the legacy regimes that dominated the Cold War era. These regimes were multilateral, targeted, and designed to manage shared national security priorities rather than shape wider geostrategic outcomes. Key examples include:

The Wassenaar Arrangement: Established in 1966 by 22 co-founding countries including Russia, the US, and most European nations, the Wassenaar Arrangement now includes 42 member states. It covers 22 categories of munitions, including tanks, aircraft, missiles, and a list of dual-use technologies, including electronics, telecommunications equipment, and surveillance tools.

The Australia Group: Founded in 1985 after Iraq’s 1984 deployment of chemical weapons by 15 founding countries, the Australia Group now includes 43 member states and covers chemicals, biological agents, and dual-use production equipment related to the production of chemical and biological weapons.

While these regimes still formally anchor the global control system, their practical relevance has declined. Within the Wassenaar Arrangement, Russia has frequently vetoed proposed controls on technologies relevant to its military capabilities since 2022 while reportedly leveraging regime information-sharing mechanisms for intelligence collection. Proposed solutions such as “Wassenaar minus one,” which imply that the regime can only remain functional through the removal of obstructive members, underscore the declining viability of true multilateral harmonization. As consensus-based coordination erodes, major powers are already increasingly relying on unilateral regimes, accelerating both fragmentation of export control application and their use as instruments of offensive statecraft.

The US export control approach

Since 2019, US export controls evolved from targeted firm-level restrictions to broad, extraterritorial application aimed at preserving US technological advantage over China. This approach relies not only on leveraging US dominance in semiconductor design, but also coordination with or pressure on allies to align their own export restrictions with US objectives. Led by the Department of Commerce’s Bureau of Industry and Security (BIS), US export controls combine Entity List designations restricting imports to specific foreign firms, end-use restrictions targeting military applications, and Foreign Direct Product Rules (FDPR) extending US jurisdiction to foreign-made products made with US components.

The 2018 Export Control Reform Act expanded presidential authority to place export controls on dual-use “emerging critical technologies,” enabling more flexible, economic security-driven controls beyond traditional non-proliferation frameworks.

In 2019, BIS placed Huawei and 68 affiliates on the Entity List, then in 2020 expanded the FDPR to require licensing for foreign-made semiconductor components produced with US technology if destined for listed entities. These steps effectively globalized the scope of semiconductor export control enforcement, notably affecting manufacturers in Taiwan, Japan, South Korea, and the Netherlands.

In October 2022, concurrent with the CHIPS and Science Act, BIS imposed sweeping restrictions on exports of advanced logic and memory chips, semiconductor manufacturing equipment, and items with supercomputing end-uses to China, securing parallel commitments from Taiwan, Japan, and the Netherlands in January 2023. These steps solidified a decisive transition from a reliance on firm-level restrictions to ecosystem-wide denial.

BIS’ January 2025 AI Diffusion Rule – the most aggressive of Biden-era export restrictions – expanded global controls on AI chips, model weights, and compute infrastructure, dividing counties into three tiers with varying access levels; approximately 120 nations became subject to licensing caps, and 25 were fully embargoed.

The second Trump administration has been transactional in its approach to export controls with China, cancelling the Biden-era AI Diffusion Rule, greenlighting Nvidia H200 chip sales to China (through Beijing has restricted imports to protect domestic industry), and pausing the BIS “Affiliates Rule” in response to Chinese rare earth pressure. BIS’ February 2026 $252 million settlement with California-based semiconductor manufacturing equipment producer Applied Materials for unlicensed exports to China (the second-largest in BIS history) underscores that while policy signaling may fluctuate, compliance obligations remain strictly enforced. USTR Jamieson Greer noted that semiconductor controls were not a major point of discussions by the leaders at the May 14-15 summit, though Trump did confirm again the US willingness to permit the sale of Nvidia’s H200 chip to approved Chinese companies.

China’s export control approach

Since 2020, Beijing has developed a more flexible and operational export control framework broadly modeled on the US approach, including a unified Export Control Law and the Unreliable Entity List, enabling increasingly coercive use of controls in pursuit of broader geoeconomic objectives. Much of China’s new legislation is a direct challenge to what it believes extraterritorial actions taken by the US and Europe to damage China’s access to key technology, especially the advanced machinery necessary for the production of semiconductors.

China’s 2020 Export Control Law established its first comprehensive national export control framework, including a control list system, supervision mechanisms, and more comprehensive coverage of goods, technologies, and services, replacing a system of fragmented, sector-specific regulations. The Unreliable Entity List (UEL), also introduced in 2020, created a mechanism to restrict foreign firms’ trade, investment, and operation in China.

In April 2025, in response to US “Liberation Day” reciprocal tariffs, China placed controls on seven rare earth categories, targeting compounds relevant to aerospace, defense, and semiconductor application, with controls expanded to five additional categories in October (China then paused application of these expanded controls by one year in November). While structured as licensing requirements rather than export bans, the measures effectively countered US controls on leading-edge compute by limiting access to critical upstream rare earth inputs, also affecting key third-party importers such as the EU.

China’s Ministry of Commerce (MOFCOM) added 76 entities to the UEL in 2025 – a jump from three additions in 2024 and two in 2023 – with a focus on US defense, drone, and technology firms. Despite de-escalatory steps in November 2025 that saw 15 US firms delisted, MOFCOM’s operationalization of the UEL demonstrated China’s willingness to begin applying the new export control mechanisms in a tit-for-tat retaliatory manner amid geopolitical disputes.

Following the May 14-15 Trump-Xi summit, US officials said Beijing was complying with rare earths export licenses as agreed to last November, but the reality on the ground is that US end-users continue to report that China is slow walking licenses.

The EU export control approach

Brussels’ hybrid export control architecture, combining common bloc-wide standards with member-state-led implementation, lacks the offensive reach of the US global denial regime or China’s coercion-focused model. Historically, the EU relied heavily on US export control enforcement to achieve technology denial aims, enabled by substantial overlap in geopolitical priorities. That alignment is increasingly fraying, particularly following Russia’s invasion of Ukraine, wavering US support for Kyiv, and US threats to Greenland. Recent steps to improve member-state coordination reflect growing aims to leverage export controls more strategically.

The EU Dual-Use Regulation, last updated in 2021, governs exports of civilian goods and technologies with potential military application and forms the basis of the union’s multilateral export control model. The 2021 update expanded enforcement coordination among member states and introduced “catch-all” controls for cyber-surveillance products, requiring producers to acquire export licenses based on end-use, even if non-listed. In December 2022, the EU appointed its first special envoy for sanctions implementation, marking recognition of the need to harmonize and strengthen the bloc’s sanctions enforcement capabilities.

While not legally binding, the 2023 European Economic Security Strategy emphasized the need for more “coordinated action at EU level in the area of export controls,” discouraging member states from adopting unilateral controls without union-wide buy-in.

The European Commission’s 2024 White Paper on Export Controls and subsequent adoption of the 2025 Recommendation on National Control Lists introduced mechanisms to facilitate greater for member-state coordination on national control lists, including information sharing before new controls are adopted.

While not a formal export control measure, the December 2023 adoption of EU Anti-Coercion Instrument reflects the Brussels’ broader efforts to develop more centralized and autonomous geoeconomic levers. The instrument, which is yet to be used, authorizes the EU to impose retaliatory measures, including tariffs and limits on market access, against “economic coercion” by non-EU states.

Implications for geopolitical dynamics

The rapid expansion of unilateral, geopolitically driven export controls shows that major powers increasingly view economic interdependence as a source of strategic vulnerability and leverage. Governments and firms alike are under growing pressure to identify and hedge against global chokepoints in critical technology supply chains, contributing to a gradual shift toward more politically resilient economic architectures built around more expansive controls. This trend will play an increasingly important role in shaping relations among the US, the EU, and China.

General US-EU export control alignment is likely to hold, but selective divergence to become increasingly plausible as Brussels expands unilateral capabilities. A full break on top-line export control priorities remains unlikely given shared core concerns over dual-use technology transfers to China and Russia. However, Brussels is likely to become less willing to mirror US controls perceived as retaliatory measures tied to bilateral US-China disputes, particularly where such actions increase European exposure to Chinese countermeasures such as rare earth restrictions. China’s critical mineral controls have demonstrated that US-China export control escalation can impose significant downstream costs on Europe, with greater autonomy over export strategy allowing Brussels to create greater distance from future retaliatory cycles.

Export controls also continue as frontline bargaining instruments in the US-China relationship after leaders fail to signal restraint at summit. A transactional environment in which export control application will fluctuate with the state of broader negotiations will mark a continuation of the approaches practiced by both sides since the start of the second Trump administration. The elimination of Trump’s IEEPA tariff powers could entice him to lean heavier on export controls as a source of leverage, though he does this at some peril given China’s willingness to play hardball with export licenses for rare earths.

Sanctioned states will enhance cooperation to blunt impact of expanding regimes. Russia’s wartime reliance on Iranian drones (reciprocated by Russian deliveries to Iran during the current war) and North Korean artillery and troops demonstrates how sanctioned states are already pooling resources to counter growing restrictions. China, while more cautious, will likely continue to play an enabling role through financial and trade connectivity to help sustain these relationships. It is also less willing to comply with US sanctions policies it views as unfair, invoking a 2021 “blocking rule” to instruct Chinese refiners not to comply with US sanctions on Iranian oil exports.

Implications for global business

The expanding scope and growing geopolitical use of export controls are making the global business environment more restrictive and volatile. For multinational firms, the core compliance challenge is not only that more products are becoming controlled but also that the pace, scope, and geographic focus of restrictions are increasingly shaped by strategic competition. This weakens the predictability that has traditionally supported long-term investment in globally integrated operating models while also increasing compliance costs.

Corporate neutrality becomes harder to maintain. Fragmentation will make it increasingly difficult for multinationals to operate as commercially neutral actors across competing regulatory regimes. A firm that complies with US restrictions may face Chinese retaliation; a firm that maintains Chinese exposure may face US or EU scrutiny; and a firm that routes through third countries will face anti-circumvention enforcement. Space for firms to serve all major markets under a single governance structure is narrowing.

Technology flows to become more regionalized. As controls expand beyond physical goods to encompass software, technical data, and compute access, cross border R&D collaboration and technology transfer will become more constrained. Firms will feel pressure to secure regionally or nationally bounded supply chains and innovation ecosystems to avoid unexpected restrictions on cross-border technology transfers, reducing scale efficiencies and slowing the global diffusion of high-end technology.

Pre-emptive decoupling to become defining feature of compliance behavior. If this direction continues, firms will face pressure to increasingly restrict activities in advance of formal regulation to avoid exposure. This chilling effect will reduce market participation and amplify the real economic impact of export controls beyond their formal legal boundaries.

| A guest post by

|